As the Federal Reserve moves through its rate-cutting strategy, mortgage companies are seeing their yields tighten in real time. What made these loans so profitable when rates rose, their floating rate, is now a struggle for borrowers as mortgage rates fall.

Mechanics of squeezing

Most loans in these sectors are tied to floating benchmarks, particularly the 3-month Secured Overnight Financing Rate (SOFR). When the Fed hikes, the SOFR rises, and borrowers charge higher interest rates. When the Fed cuts, the opposite happens.

New businesses coming out today are also coming in with lower credit spreads than companies were able to command during the boom. The base rate is decreasing, and the price above that rate is also decreasing.

Diabetes from a very long time

During the interest rate crisis, many mortgage loan managers offered various types of relief to borrowers struggling with the burden of paying large amounts of debt. These measures, which may include transfer of payments, modified terms, or other controls, were a way to prevent portfolios from showing cracks. These support systems continue to improve performance even as the environment changes.

The weak labor market has led the Fed to tighten recently to slow job growth. A company that had already started paying off its debt at high rates will not be healthy because its interest rate will drop by one or two percentage points.

The average price is still there, but the difference is narrowing

Despite declining yields, private equity remains more valuable than other bond options. Investors still get more credit through a private equity fund than they would through a stock or high-yield bond in the public market.

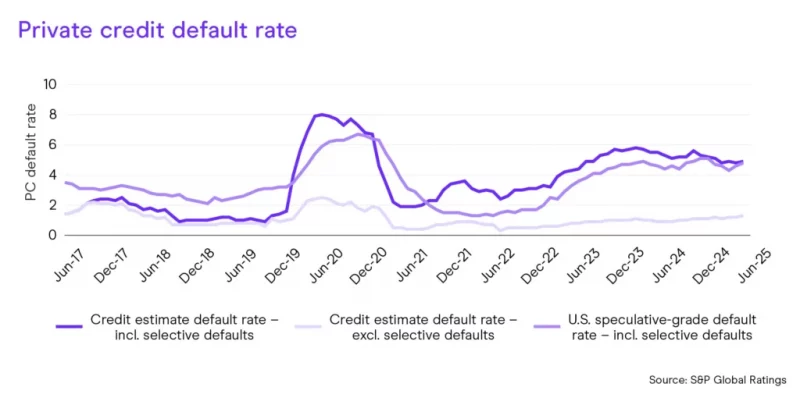

The risk that deserves the most attention is the intersection of low yield and high volatility. If the recession that led to the Fed’s rate cuts leads to lower credit among borrowers, credit bureaus may face lower returns on loan repayments while simultaneously incurring losses on defaulters.