Wall Street analysts and forecasters have offered mixed opinions Nvidia (NASDAQ: NVDA) stock at the end of 2026.

Of course, most forecasts focus only on economic growth artificial intelligence architecture and release of next-generation platforms such as Blackwell and Rubin.

Nvidia’s increased data center investment and leadership in parallel computing also supports the view of many analysts.

Despite the increase in volatility, NVDA shares have recently moved in line with the market’s broader sentiment, which remains, fueled by rising international tensions in the Middle East.

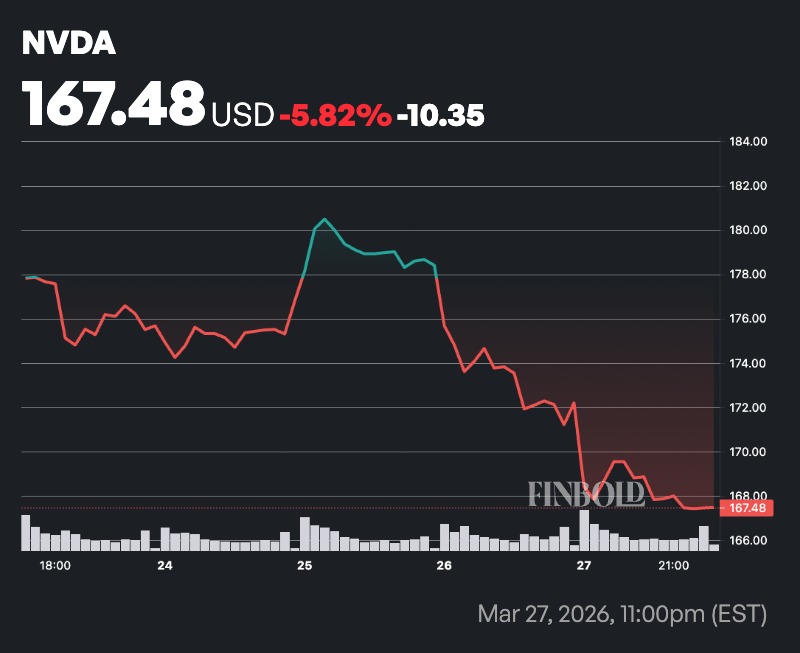

As of press time, Nvidia stock was valued at $167, down more than 11% year to date.

The lowest price of Nvidia Stock Exchange shares

Among these indicators, Evercore ISI analyst Mark Lipacis keeps the main goal at $352 by the end of 2026. The company has also confirmed that it is ‘Outperform’, referring to the growth of income that can reach 79% by the middle of 2026, the great demand for AI accelerators, and the spread of all software, network use, commercial transfer, and transfer.

Dan Ives of Wedbush Securities suggested a $250 share for December 2026 to late 2025, based on annual gains of 15% to 20% during the AI build. Following the strong benefits are GTC updatesraised his bullish target to $300, pointing to Nvidia’s technology front and expanding AI use cases.

Major banks, including Bank of America, Citigroup, and JPMorgan Chase, also show that Nvidia will be close to $ 300 by the end of 2026. These figures show expectations of more than $ 1 trillion in the use of increased data through 2027, the rapid implementation of AI, and other improvements from new platforms.

An independent analysis adds a similar estimate. On that line, Keithen Drury is making a price of $309 based on 2027 earnings per share of $7.74 and a 40x forward earnings ratio.

Nvidia stock tailwinds

In the forecast, analysts highlight key factors such as hyperscaler spending, the shift from education to workloads, AI initiatives, emerging market demand, and Nvidia’s ability to command premium pricing through its entire ecosystem.

At the same time, the growth of money for semiconductor The giant is expected to decline from its recent peak but remain strong, with economic estimates for 2027 of around 60% to 65% per year.

Risks include a decline in AI investment, increased competition in conventional silicon, supply stability, geopolitical pressure on China’s exports, and lower prices if growth does not meet expectations.

Image courtesy of Shutterstock