This is an excerpt from the 0xResearch newsletter. To read the full article, register.

Over the past few days, the exchange between Kamino and Jupiter has escalated from a friendly rivalry to a public feud. The events began on Nov. 27, when Jup Lend introduced a refinancing tool in front of him to move the slope from Kamino Multiply directly to Jup Lend with just one click. The reformulation process introduced an atomic function with four steps:

- Bring back the remaining credit on Kamino.

- Remove the collateral.

- Send these items to Jupiter Lend.

- Renovate the property within Jupiter Lend, and keep the same amount and collateral.

On Dec. 2, Kamino has been changed its smart contracts to cancel the Jupiter program, one click cancellation. Both Jupiter and Fluid (Jup Lend uses Fluid in the background) have framed the move as anti-competitive and against “open finance principles.”

On December 6, the co-founder of Kamino publicly he explained for banning Jup Lend’s migration tool, noting that Jupiter has repeatedly stated that borrowers’ collateral should be independent, meaning that it is not duplicated or at risk of infection. However, these claims were not true, even by the co-founder of Fluid acceptance Replication within Jup Lend.

In particular, Kamino did not prevent users from paying off their loans manually and withdrawing their money from Jup Lend. Whether it goes against the principles of open finance or not, the move to restrict the refund program was a business decision, just like Jup Lend’s decision not to open source its code (although it has plans to do so). For this reason, it is interesting to analyze the performance of the financial markets in the last few months.

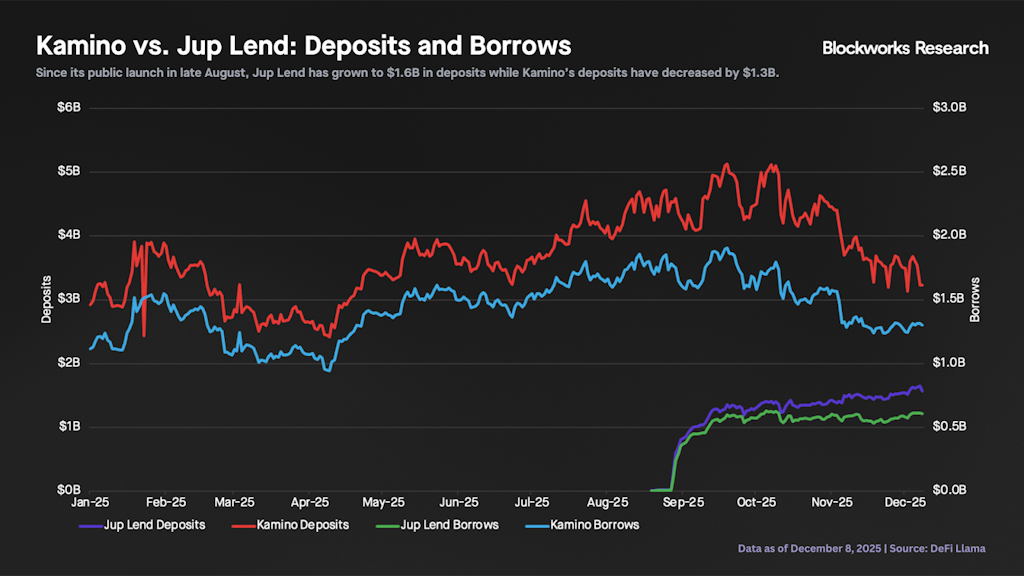

Since its launch in late August, Jup Lend has grown to $1.6 billion in deposits and $610 million in loans. The chart below shows that Kamino’s deposits and loans decreased by $1.3 billion (-28%) and $460 million (-26%), respectively, during the same period.

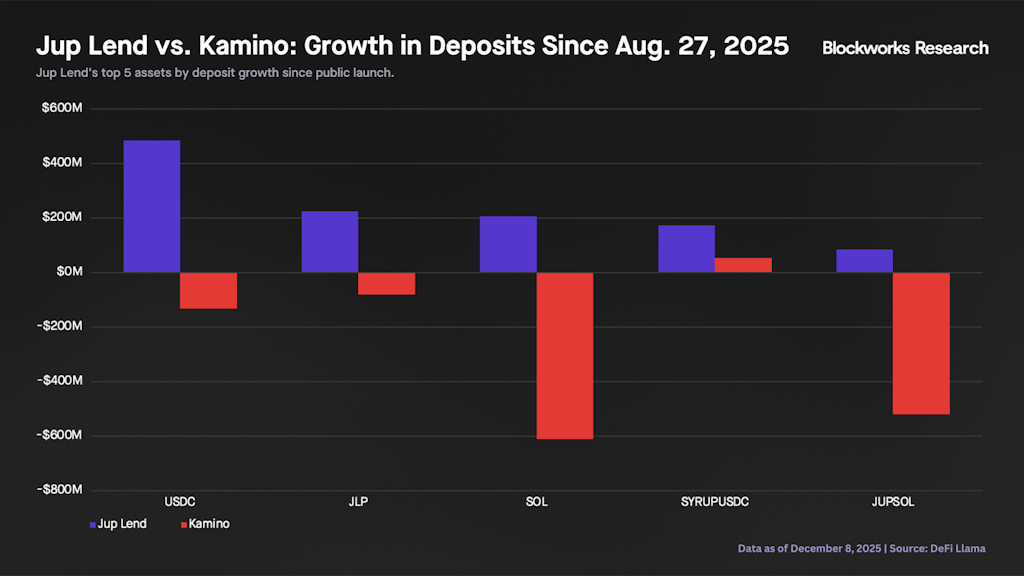

The top five factors in deposit growth since the launch of Jup Lend are USDC ($485 million), JLP ($225 million), SOL ($206 million), syrupUSDC ($174 million), and jupSOL ($85 million). At the same time, Kamino saw a large outflow of all of these products, except syrupUSDC. However, despite syrupUSDC, Jup Lend still attracted almost 3x more.

Kamino’s growth in the past few months has come from sources that were not supported by Jup Lend. In particular, stablecoin penetration in Q4 has been driven by PYUSD ($42 million) and Phantom CASH ($125 million). Kamino has also been active in boarding DATCO LSTs; especially dfdvSOL and fwdSOL recently.

PRIME integration of Kamino is seen as a catalyst that can bring new money to the financial market. PRIME offers users access to a regulated loan with US mortgages originated and financed through Image. This combination provides an opportunity to obtain yields unmatched by the crypto markets that will attract many borrowers.

Finally, Kamino and Jup Lend are obviously competitors, and competition is healthy because it drives innovation and ultimately benefits users. This has been reported, as Lily Liu of the Solana Foundation he realizedInstead of fighting each other, Kamino and Jupiter should think about growing the pie and taking market share from other chains and TradFi later. In addition, all financial markets are still less than 10% of Aave’s deposits, and without initiatives like the integration of PRIME, it is not possible to close this gap.

Get news in your inbox. Check out the Blockworks blog post: