Author

Ahmed Barakat

Author

Share it

Facts Checked by

CryptoNews Editorial Team

Author

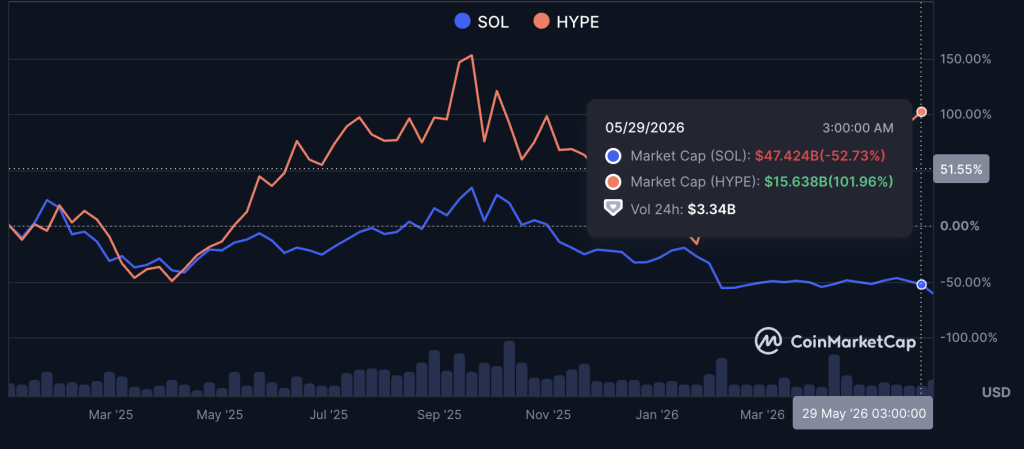

Hyperliquid (HYPE) is outperforming Solana (SOL) in value, and the gap is widening. SOL has fallen to its lowest level since 2023, shaken by the DeFi cycle from L1S, while HYPE has taken the transferred capital and continued to rise.

But rising prices and controlling the market cap are different meats. Solana’s circular market is still above $ 38 billion, supported by infrastructure, CME futures, ETF flows, and Tier-1 collateral for all major transactions, which Hyperliquid has not made and cannot quickly repeat.

A conversion story is as real as a business idea. As a result of recent development, it is not permanent.

Note: The best crypto to change your profile

Solana vs. The Hyperliquid Liquidity Moat Is Not A Rhetoric, It’s A Reality

The difference in crypto customers between the two products is not insignificant. Solana acts as a bridge between central exchanges, institutional capital, and emerging ETFs.

That interest rate refers to the buying pressure that exists without reference to specifications.

Hyperliquid is a permanent DEX, a highly optimized trading chain. It works very well.

But private equity and platform assets are priced at completely different rates, and historically, fixed-income shares are more expensive than single-purpose real estate.

The FDV trap is also real. More and more estimates are based on the Hyperliquid’s liquid price rather than market volatility.

For HYPE to pass the SOL cycle, it will need to maintain current prices as its float increases over the next 2 to 4 years, the problem of disrupting Solana is already past the post-2022 rebuild.

Consider liquidation asymmetry. A $1.1 billion market liquidation event that contributed to SOL’s decline to 2023 declines and Hyperliquid’s risk assessment.

The HL protocol survived, but this unit proved that its resilience is still being established in real time, while Solana’s depth can absorb such instability without structural damage. Understanding how capital rotation dynamicscs moves between group contexts here; the money that goes into HYPE is not the same as the money that goes into building a revolving fund.

Solana’s online presence runs deeper than marketing. The integration of Visa, DePIN protocols, thousands of applications, this creates a variety of payment methods and a natural stability that a focused AppChain cannot duplicate. S

OL costs do not decrease if output volume decreases by 40%. The economic theory of HYPE is based on almost constant demand.

The Hype Bull Case Is Hard, Don’t Lose It

Arthur Hayes has publicly argued that HYPE can outperform SOL before the bull cycle ends, relying on Hyperliquid interest rates and the strength of demand.

However, at the time of writing, he published a post saying that he had lost all his possessions.

The idea of the company Syncracy Capitals Daniel Cheung created Hyperliquid as “a large chain where trading activities are taking place” and a place “to bring new users into crypto right now”, to mention its 24/7 markets as a design opportunity rather than a place constrained by traditional market times.

The mindshare argument is valid. The protocol becomes an unstable environment for the traders involved, which creates many problems that are difficult to remove.