Author

Ahmed Barakat

Author

Share it

Sam Altman, ChatGPT AI, just put a white number on SpaceX’s price predictions, and see the post-IPO drag as an entry point rather than a warning sign. The model predicts $225 by the end of 2026, which is about 55% from where shares are today, and $250 or more if growth continues.

The bull case puts everything to money that many investors have yet to fix. SpaceX is expected to make $18.7 billion in revenue in 2025, with Starlink contributing nearly 60% of the total, meaning that the Internet-only business brings in more annual revenue than most mid-sized tech companies.

The combination of broadband, aviation, security, and exposure to AI development in a single ticker is truly rare and that is what this model points to in order to prove its value proposition.

Starlink’s subscriber base is growing with recurring revenue increasing every quarter. SpaceX maintains an unparalleled cadence that no competitor has come close to matching. Starship continues to advance for reusability, and the advanced AI opportunities associated with satellite communication and computing at the edge add new growth on top of the existing business.

Together, these factors contribute to the re-introduction after which these types of frameworks act as a natural form of IPO rather than a major problem with the business.

The bear case identifies three specific risks rather than vague concerns. A major Starship delay would reduce the utility’s assumptions that justified many of the long-term costs. Excessive pressure from AI investments on profit generation can squeeze opportunities faster than investment growth can slow them down.

And investors rejecting a price that remains too high compared to what it’s currently selling for is the easiest and most recent risk, since SpaceX went public at an already inflated price in the years ahead. Under these conditions, the brand sees the shares moving towards $110 to $120 instead.

SpaceX Price Prediction: SpaceX Hits Its IPO Bottom With $225 Target Staying High

The 3-hour chart shows SpaceX at $145.35 after a significant decline from its IPO-week high near $219, which is in mid-June.

The entire move from the IPO rise to current levels has taken less than a month, which is the type of IPO-style violence that occurs when quick buyers take profits and get excited about sales colliding with the reality of the stock price.

The price has been steadily declining since the June 17 peak, with each attempt to make a new low before rebounding.

The most recent meetings from July 8 to 10 have been very weak, and the stock has lost a little and is now trading near the lowest since the IPO was opened.

The first resistance is near $155, the level that made the most recent test at the beginning of July, and the heaviest ceiling near $173, where the combined area later remained for a few days before falling. Support is near $145, an available test point, and the lowest the stock has traded since going public.

Below, there is no clear technical area available on this chart because the IPO history is too short to generate initial support. The general method here is the recent distribution of the IPO, which uses stocks every day since the first rise to work quickly instead of building any kind of base.

Momentum looks weak and still points below the 3-hour candlestick, sellers are controlling all of the recent trades. In order for the $225 bull case to be technically necessary, SpaceX would have to first stop the cost reduction, return the $160, and keep the many issues that are driven by the money that ensures that Starlink gets the money that the brand depends on.

Don’t miss our $1,000 USDT Airdrop on ByBit

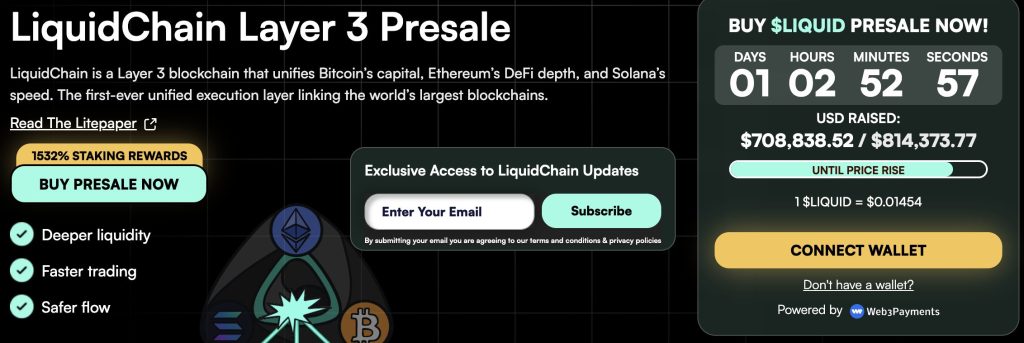

LiquidChain Attracts SpaceX Owners’ Interest: ChatGPT AI Predicts 100x Success

The cycle is already underway. Most people only look back.

Large-cap crypto does not fail. It’s a hat. BitcoinEthereum, and XRP have been fighting the same opposition groups for weeks. Macro tailwinds are slowing down.

Corporate income continues into the next quarter. Keeping a stock where the highs are dependent on the raw materials you can’t control is not an option. It’s waiting.

A capital that has traveled around enough does not wait for rejection. It moves without a destination in sight.

Basic construction games work on different maths. A less efficient market means that less volatility results in greater price movements. The asymmetry exists because the market has no value for what is currently being built. This difference between the actual valuation and the actual value of the project is where the returns come from.

Multiple chain splits cost DeFi real money every day. Bitcoin, Ethereum, and Solana run isolated systems without a connection mechanism. Any user moving between the environment incurs a direct cost in fees, downtime, and downtime.

LiquidChain breaks all 3 networks into one killer platform. One delivery. Full access to nature. There is no cross tax on any transactions.

The market hasn’t figured this out yet. That’s the whole point.

Trading is already at $0.01454 with only $820,000 raised. Bottom line is not a marketing term here. That is the explanation where this is in his life.

Execution is not guaranteed. Adoption is unknown. The risks are real and should be specifically mentioned. The installed load provides easy access to the roof that is already visible. This gives the former a seat at the table that hasn’t been set yet.