Strategy can use its Bitcoin liquidity to support its earnings and demand and increase its holdings, CEO Michael Saylor said during the company’s May 5 earnings call.

Show it @StrategyThe Q1 Earnings Call is here on X. We’ll start again:

-Q1 economic results

-Digital Currency $STRC

-Digital Equity $MSTRFollowed by a live Q&A!https://t.co/j4rKKAvU0A

– Strategy (@Strategy) May 5, 2026

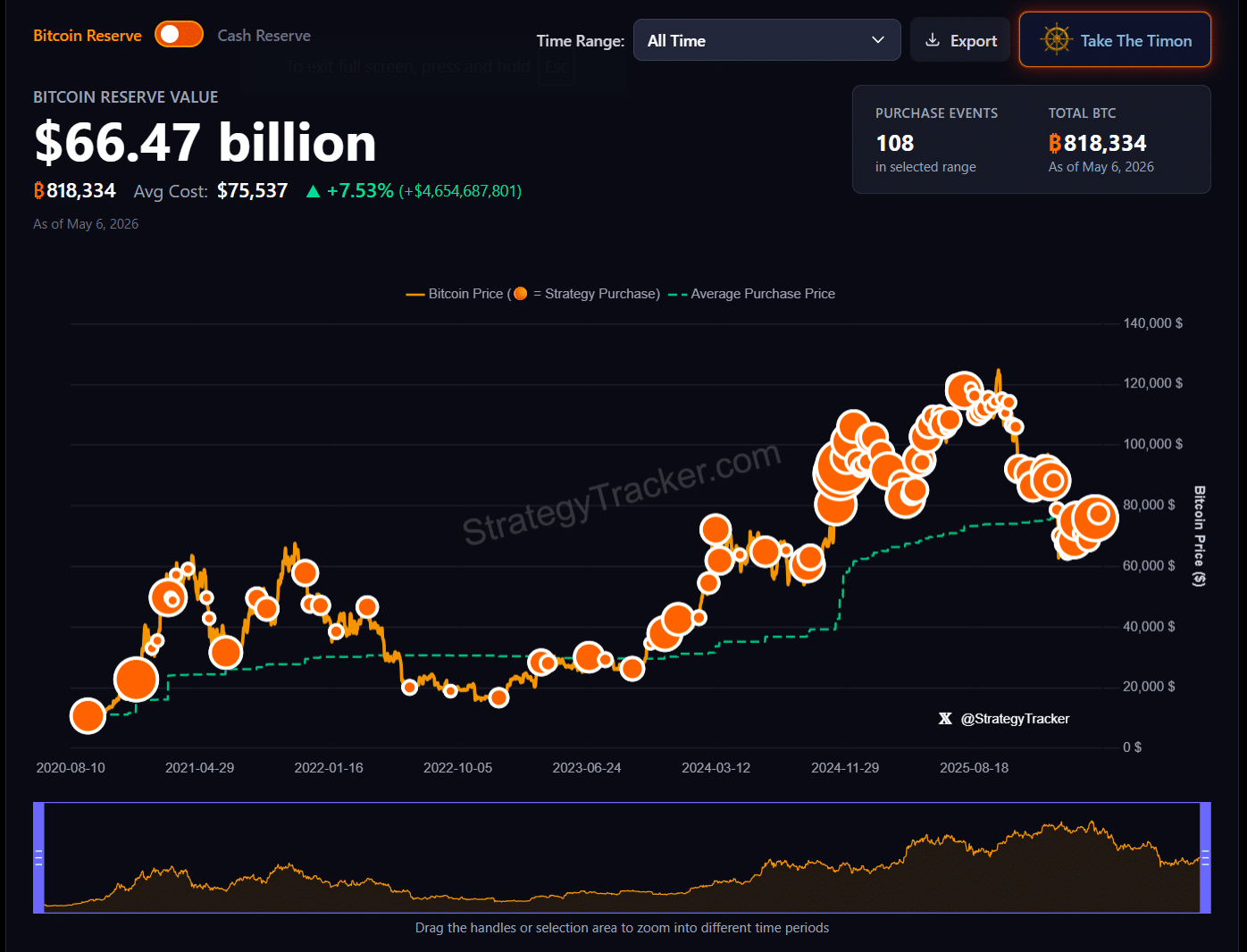

The largest Bitcoin company has acquired 818,334 BTC, which is worth about $67 billion. With Bitcoin hovering around $81,500, the company is worth about $4.6 billion on paper.

Explaining the company’s capital framework, Saylor pointed to Bitcoin’s breakeven annual return of about 2.3%. Above this level, Strategy can pay its dividends by selling Bitcoin while still growing its entire Bitcoin portfolio, thanks to the strong leverage from STRC.

In other words, the brand is managed by offering STRC, the company’s favorite tool, and investing the money in additional Bitcoin. When output exceeds the limit, new coins are raised more than what Bitcoin sells for profit, causing Bitcoin to increase over time.

“We can stop selling MSTR, our common stock right now. We can pay the payment and trade in Bitcoin. And if the Stretch issue is greater than the BTC breakeven number, not only will we pay dividends forever, we will increase the amount of Bitcoin we have forever at the same time,” said Saylor.

“If we can sell $1.5 billion of Stretch per year, we can sell Bitcoin, pay dividends, buy more Bitcoin than we sell, increase our Bitcoin investment and generate Bitcoin yield,” he added.

At the 20% annual rate of STRC output, Saylor’s services the company can accumulate 144,000 Bitcoin in a year, even if it pays all the money through Bitcoin sales only and not using all the markets.

“You buy Bitcoin with credit, you let it appreciate, and then you sell Bitcoin to make payments,” Saylor said. “As long as you’re over-lending, this business will work and grow forever.”

In bolstering the argument, Saylor compared the Strategy to a real estate developer who buys land for $10,000 an acre, sells it for $100,000, and recoups the money. He said this does not disrupt the market but shows the distribution of wealth.

“We are like a Bitcoin development company. We buy it cheap, we sell it dear,” He said. “Capital gains fund credit dividends. This is the basis of business.”

“And it is clear that sometimes we will sell Bitcoin derivatives because it is very useful for the company, but it is not necessary,” he added.

Opinion, however, is centered almost entirely on Bitcoin’s long-term appreciation. Saylor’s conservative model assumes that the stock appreciates about 10% annually, in line with the historical S&P 500. His base case assumes 30%.

By any measure, Bitcoin’s medium-term trading is not allowing for market pressure but is a deliberate part of the mechanism designed to continue to accumulate the asset as it fulfills its mandate, according to Saylor.

Strategy has maintained strict no-trade rules for Bitcoin under its asset management strategy, increasing its holdings through the capital markets and standing firm.

Saylor pushed back against “short stories” that show that Bitcoin trading is wrong or evidence that the Strategy model is wrong, but this will not completely eliminate the perceived risk in the market.

The Strategy’s value is largely driven by the long-held belief that the company rarely sells Bitcoin. Even a good, well-defined sale can still cause short-term stress.

Shares of the company fell in the short-term trading session, while Bitcoin settled above $81,000.